It can be hard to keep track of your money. For a lot of people, it feels like they are always juggling bills, spending money on things they don’t need, and saving money. The hard part is finding a way to live in the moment and plan for the future at the same time. If this sounds familiar, the 50/30/20 rule could be the easy and useful plan you’ve been looking for. This framework is meant to make budgeting easy, useful, and long-lasting, so you can save smarter without having to deal with complicated spreadsheets or financial jargon.

What does the 50/30/20 rule mean?

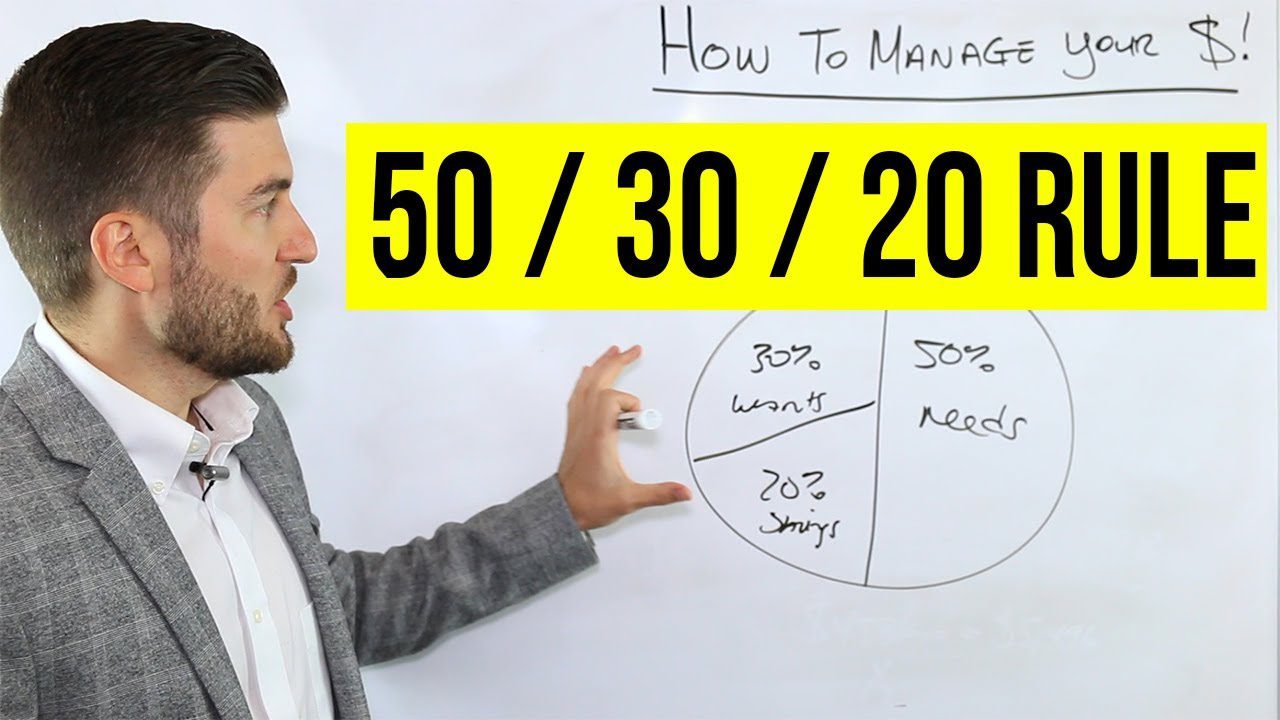

Senator Elizabeth Warren came up with the 50/30/20 rule as a way to budget in her book All Your Worth: The Ultimate Lifetime Money Plan. The idea is simple: spend 50% of your after-tax income on needs, 30% on wants, and 20% on paying off debt and saving. By taking this approach, you make a balanced financial plan that includes all of your needs, gives you room to have fun, and keeps you moving toward your financial goals.

50% of your income goes to understanding your needs.

You need the first half of your income. These are the costs that you have to pay and that are necessary for keeping your life stable. This includes your rent or mortgage, utility bills, groceries, transportation costs, health insurance, and any debts you have to pay. If you keep your basic costs to less than half of your income, you can live your daily life without feeling like you’re in a financial bind. It also makes you think carefully about how you spend your money. If your basic costs are always higher than this limit, it might mean you need to rethink some of your lifestyle choices, like moving to a cheaper home or finding ways to lower your utility bills.

30% of your income goes to balancing wants.

The next 30% of your money is set aside for things you want. Wants are things that make your life better but aren’t necessary for survival. This category lets you spend your money freely without putting your financial stability at risk. Eating out, going to the movies, going on vacation, doing hobbies, and other optional spending are some examples. Setting aside a certain amount of money for wants lets you treat yourself without going overboard, and it stops you from spending too much or too quickly by giving you a clear limit. If you notice that your discretionary spending is consistently over thirty percent, it might be time to rethink your priorities and make sure that having fun doesn’t hurt your finances.

Saving Smarter: 20% for paying off debt and saving

The other twenty percent goes toward paying off debt and saving. This part is probably the most important for keeping your money safe in the long run. Setting aside this part of your budget for things like building an emergency fund, putting money into retirement accounts, paying off high-interest debt, or investing can give you a financial safety net that can help you in tough times. Even small, regular contributions to savings or paying off debt can have a big effect over time because of the power of compounding. By making this a must-have in your budget, you learn to put future stability ahead of present enjoyment.

How to Use the 50/30/20 Rule

To use the 50/30/20 rule, you first need to know how much money you make after taxes. This is the amount of money you actually bring home each month after taxes are taken out. Now that you know this number, you can start to group all of your spending into needs, wants, and payments on debts or savings. The most important thing is to be honest about what you need and what you don’t need. You can change your habits to fit the 50/30/20 framework once you know exactly how much money you spend. By making a structured but flexible budget, this method can make it easier to make financial decisions and lower stress over time.

The 50/30/20 Rule has these benefits:

One of the best things about the 50/30/20 rule is that it can be changed. This method can be changed to fit your life, income, and financial goals. When you make more money, you might want to put more of it into savings or investments. On the other hand, if your expenses go up for a short time, you might cut back on things you want while keeping up with your savings and contributions to your basic needs. Because it is flexible, this rule works for a lot of different lifestyles and financial situations.

Its simplicity is another plus. A lot of people are scared of budgeting because they think it means using complicated spreadsheets, apps, or keeping an eye on things all the time. The 50/30/20 rule gets rid of that problem by giving you a simple, clear structure to follow. You can quickly see how your money is being spent and where you might need to make changes by splitting your income into three groups. It also encourages people to plan ahead for their finances, which lowers the risk of getting into debt and gives them a sense of control over their money.

Questions that come up a lot

What if my basic costs are more than half of my income?

If your needs take up more than half of your income, you might want to look at your living situation, how you use utilities, or how you get around. To keep spending in check, you might need to downsize or look for cheaper options.

Can people who don’t make a lot of money use the 50/30/20 rule?

Yes, it can, but you need to be flexible. People with low incomes may need to put their savings and necessities in a different order. You can change the percentages, but the idea of balancing needs, wants, and savings should stay the same.

How can I stick to the 30% I set aside for wants?

Keeping track of your extra spending and setting clear limits can help. Don’t buy things on a whim; instead, plan ahead for things you don’t need. It can also be easier to keep track of your spending if you have a separate account for wants.

Is the 20% savings goal enough to plan for retirement?

Twenty percent is a good place to start, but you may need to give more depending on your retirement goals and when you want to retire. Even if you have to make changes over time, being consistent and saving early are very important.

If my income isn’t steady, can I still use the 50/30/20 rule?

Yes, but you need to plan it out more carefully. Figure out how much money you make each month on average and change your allocations based on that. During months when you make more money, put saving and paying off debt first to make up for times when you make less.

In conclusion

The 50/30/20 rule is a simple and useful way to budget that helps you keep your finances in balance. You can cover your needs, enjoy life responsibly, and build a secure financial future by setting aside 50% of your income for needs, 30% for wants, and 20% for savings and paying off debt. This simple but effective method not only helps you keep track of your money, but it also helps you develop habits that will help you stay stable and confident in your finances over time. Following the 50/30/20 rule is a step toward spending less, saving more, and, in the end, feeling better about your finances.